Owning a Home and Facing Deportation in 2025: What You Need to Know

Owning a Home and Facing Deportation in 2025: What You Need to Know Navigating homeownership is challenging under any circumstances, but the risk of deportation can make it even more daunting. As immigration policies evolve, many homeowners find themselves uncertain about their future. If you or so

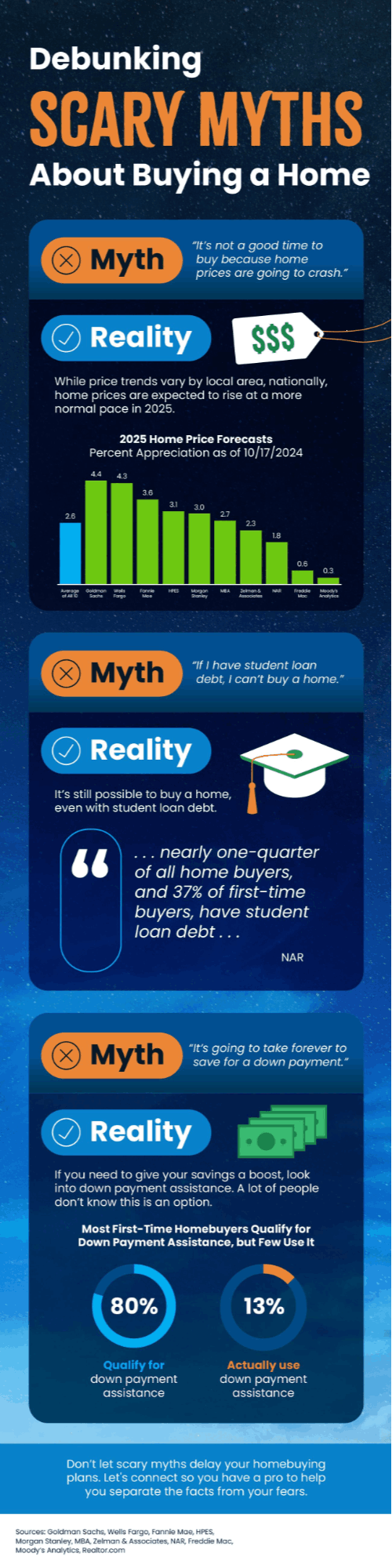

Today’s Biggest Housing Market Myths

Have you ever heard the phrase: don’t believe everything you hear? That’s especially true if you’re thinking about buying or selling a home in today’s housing market. There’s a lot of misinformation out there. And right now, making sure you have someone you can go to for trustworthy information

Unlocking Homebuyer Opportunities in 2024

There’s no arguing this past year has been difficult for homebuyers. And if you’re someone who has started the process of searching for a home, maybe you put your search on hold because the challenges in today’s market felt like too much to tackle. You’re not alone in that. A Bright MLS study found

Categories

Recent Posts