A New Federal Policy Lowers Rates

In early January 2026, a major federal initiative shook the U.S. mortgage market. Former president Donald Trump ordered federal regulators to purchase $200 billion in mortgage‑backed securities. Federal Housing Finance Agency (FHFA) director Bill Pulte announced that Fannie Mae and Freddie Mac would carry out the purchases . Because bond prices and mortgage rates move in opposite directions, this large infusion pushed bond prices up and rates down . Within one day, the average 30‑year fixed mortgage rate fell from 6.21% to 5.99%, the lowest level since February 2023 . Though some analysts at JPMorgan Chase argued that the program’s size (about 1.4% of the $14.5 trillion mortgage market) limits its impact , the immediate drop in rates suggests it offers relief for borrowers.

This policy matters for Houston and Texas homebuyers because mortgage rates are a major component of affordability. Realtor.com estimates that a typical U.S. household needs to earn $118,530 to comfortably afford a median‑priced home ($402,500); the median household income is roughly $77,700 . Lower rates reduce monthly payments and can widen the pool of buyers who qualify for financing.

Why Houston Buyers Should Pay Attention

Houston’s housing market is predicted to enter a softening phase in 2026. Analysts expect home prices to remain flat or even decline slightly in the first half of the year . Inventory has been rising—active listings in the Houston‑Pasadena‑The Woodlands metro area grew more than 22 percent in 2025 —giving buyers more options and bargaining power. Homes now spend a median of 60 days on the market , compared with just 34 days two years ago, which means less urgency and more time for inspections . Population growth, particularly migration from higher‑cost states, continues to support long‑term demand , but the short‑term market leans in favor of buyers.

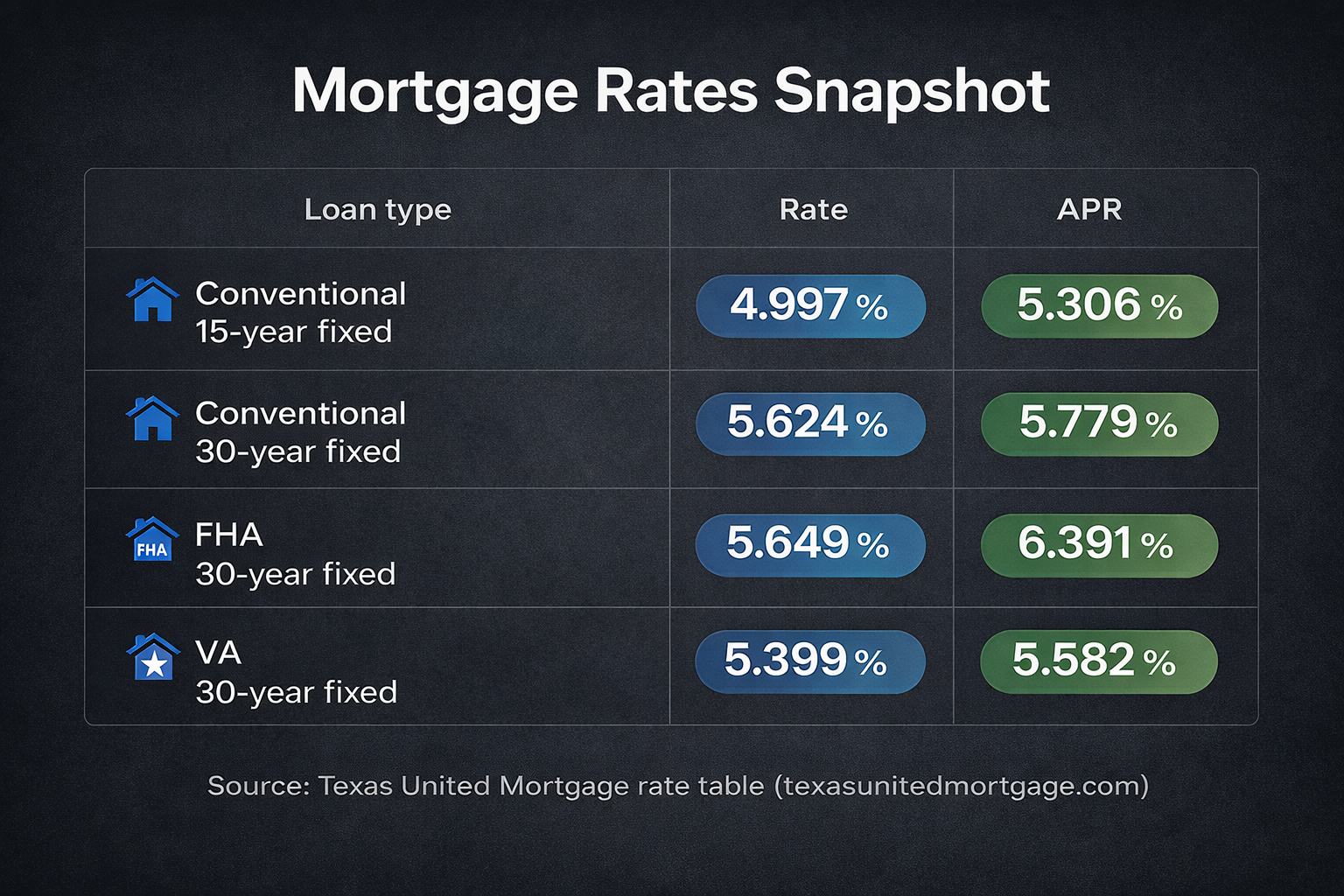

Note: Rates vary based on credit score, loan amount, and points, but they’re below the national average of around 6.1 % reported by the Houston Association of Realtors on January 29, 2026 . With the federal bond purchases pushing rates down, further decreases are possible later this year .

Local Buyer Assistance Programs

Texas offers numerous programs to help first‑time and move‑up buyers with down payments and closing costs:

Texas State Affordable Housing Corporation (TSAHC) – The Home Sweet Texas Home Loan Program and Homes for Texas Heroes Program provide 30‑year fixed‑rate mortgages with up to 5 % down‑payment assistance for credit scores 620+ . Assistance is offered as a grant or a 0 % second mortgage forgiven after three years . The Heroes program serves teachers, firefighters, EMS, police, correctional officers and veterans .

Texas Department of Housing and Community Affairs (TDHCA) – The My First Texas Home program pairs a below‑market 30‑year fixed mortgage (for FHA, VA or USDA loans) with down‑payment assistance of up to 5 % . The My Choice Texas Home program offers similar assistance with conventional loans and does not require first‑time buyer status . Both programs require minimum 620 credit scores and income limits that vary by county .

Houston’s NeighborhoodLIFT Program – Administered by Wells Fargo and NeighborWorks, this initiative gives eligible buyers up to $15,000 in down‑payment assistance (up to $17,500 for veterans, teachers and first responders) . Income must not exceed 80 % of the area median (around $59,900 for a family of four); participating buyers must take a homebuyer education course and agree to live in the home for five years .

City of Houston Homebuyer Assistance Program – Offers up to $50,000 in no‑interest, forgivable loans to buyers with household income at or below 80 % of the area median. The loan is forgiven after five years .

Veterans Land Board Housing Assistance Program – Provides low‑interest loans (often requiring no down payment) for Texas veterans and service members .

These programs can be layered; for example, buyers may combine down‑payment assistance with the federal Mortgage Credit Certificate (MCC), which reduces federal income tax liability each year .

2026 Home Financing & Housing Trends

Supply growth means leverage for buyers. Inventory in the Houston metro area sits around 4.5 months, higher than the national average . Homes stay on the market longer, giving buyers room to negotiate. Experts advise using this leverage to request seller concessions, such as a closing‑cost contribution or a buydown on your mortgage rate .

Flat or modestly declining prices. Forecasters expect Houston home prices to remain flat or dip slightly in early 2026 and then stabilize later . Zillow predicts a metro‑wide price increase of just 0.4 % from October 2025 to October 2026 .

Mortgage rates likely to drift lower. Analysts from Fannie Mae and other groups project a gradual easing of rates through 2026 . A drop from 6.5 % to 5.9 % on a median‑priced Houston home could save buyers over $120 per month .

Local market differences matter. Inner‑loop neighborhoods like The Heights remain competitive due to limited supply, while suburbs such as Cypress, Katy, The Woodlands, Waller, Crosby and Hockley offer more inventory . Slower growth areas like Sugar Land or Pearland may lean more toward buyers .

Tips for Millennials, Gen Z Buyers & Relocators

Get pre‑approved and know your budget. Use an affordability calculator and factor in not just the mortgage payment but also taxes, insurance and HOA fees. With rates around 5.6–5.9 %, every 0.1 point makes a difference.

Shop around for rates. Freddie Mac notes that obtaining quotes from three to five lenders can save thousands over the life of a loan . Local credit unions, national banks and online lenders often have very different offerings.

Take advantage of down‑payment assistance. Programs like TSAHC’s grants or Houston’s NeighborhoodLIFT can reduce the cash needed up front. Even if you have a sizable down payment, using a grant to buy down your interest rate may lower monthly payments.

Focus on neighborhoods that fit your lifestyle. For Gen Z buyers seeking walkability and nightlife, areas like Midtown or EaDo might appeal. Families may prefer master‑planned suburbs with good schools in Katy or Cypress. Research micro‑market conditions because price trends vary widely across the metro .

Consider new construction incentives. Builders in growth zones are offering rate buydowns and upgrades . These incentives can be more valuable than a small price cut on a resale home.

Prepare for a slower selling process if you’re a seller. Homes may stay on the market for two to three months . Price your home realistically and consider offering buyer incentives such as closing‑cost assistance .

Conclusion & Call to Action

The federal bond‑purchase program has nudged mortgage rates lower, offering Houston and Texas buyers a rare opportunity. Coupled with rising inventory and flat prices, 2026 could be a prime window to purchase a home in the Houston area. Whether you’re a first‑time buyer, relocating from out of state, or a homeowner looking to refinance, partnering with a knowledgeable local agent is crucial. Aurhomes Group specializes in Houston and Texas real estate, guiding clients through financing options, down‑payment assistance, neighborhood selection, and negotiation strategies. Reach out today to start exploring Houston TX homes for sale and make the most of these market dynamics.

FAQ – People Also Ask

How much house can I afford in Houston?

Affordability depends on your income, debt and down‑payment. Lenders generally use a debt‑to‑income (DTI) ratio of 43 % for FHA loans and lower for conventional loans. Use a home‑affordability calculator and get pre‑approved to understand your price range. Remember that Houston’s median home price is around $335,000 and requires a household income of roughly $90,000–$120,000, depending on the rate and down‑payment.

Is it a good time to buy in Texas in 2026?

Yes, many experts believe early 2026 presents a buyer‑friendly market. Prices are flat to slightly declining , inventory is high and mortgage rates have dipped due to federal bond buying . With down‑payment assistance programs available and rates likely to ease further , buyers have a unique window to negotiate favorable deals.

How do I qualify for first‑time buyer programs in Texas?

Most programs require a minimum 620 credit score , fall under income limits that vary by county and intend to purchase a primary residence. Completion of a homebuyer education course is often required (e.g., Houston’s NeighborhoodLIFT program ). Reach out to TSAHC, TDHCA or your local housing authority to verify eligibility.

What are the latest FHA, VA and USDA loan updates in Texas for 2026?

FHA loans still allow down payments as low as 3.5 % . VA loans remain a top option for veterans, requiring no down payment and offering competitive rates . USDA loans provide zero‑down financing for rural properties and have income limits around 115 % of the area median . All three loan types can be paired with state and local assistance programs.

Check out this article next